Even with consumer fears looking at inflation and recession, consumer spending remains strong!

The Federal Reserve Bank of New York, which regularly collects data on consumer economic sentiment, reported an increase in short-term inflation expectations on the part of consumers, but a decline in medium- and longer-term expectations. According to the Mastercard SpendingPulse, which measures in-store and online retail sales across all forms of payment, U.S. consumer retail spending, excluding automotive, rose 9.5 percent year-over-year in June; excluding auto and gas spending it was up 6.1 percent year-over-year. (http://www.greensheet.com/emagazine.php)

These are some of the trends MasterCard found in several consumer surveys:

- Consumer spending represents about two-thirds of the U.S. economy, according to the Fed.

- 51 percent of workers are short on money before they get to payday. The last time the survey was run, in 2018, it was 24 percent.

- This is not just happening with lower income consumers. Over a third of workers reporting household incomes in excess of $250,000 have found themselves in that position this year, the research center said.

- Create worthwhile promotions that brings them back

- Offer unique or rare products and services that makes you the ONLY place they want to come to purchase!

- Offer rewards and loyalty programs to keep them coming back to your business!

- Continue to offer your products and services via online website!

- Offer delivery services or drop to car pick-up

Each business today is already complaining about supply chain issues, inflation and outrages gas prices effecting their "bottomline"! But you can change that by understanding how to recapture your market and bring in happy customers!

We have some local restaurants in the south Florida area that promote via FaceBook everyweek and bring in lots of new customers by offering nice promotions! They offer a coupon for the next time they come in along with a take-home menu for them to order online or by phone for takeout or delivery!

Find a way to connect to your customers; they still want STUFF! They are just less apt to spend if you offer NOTHING!

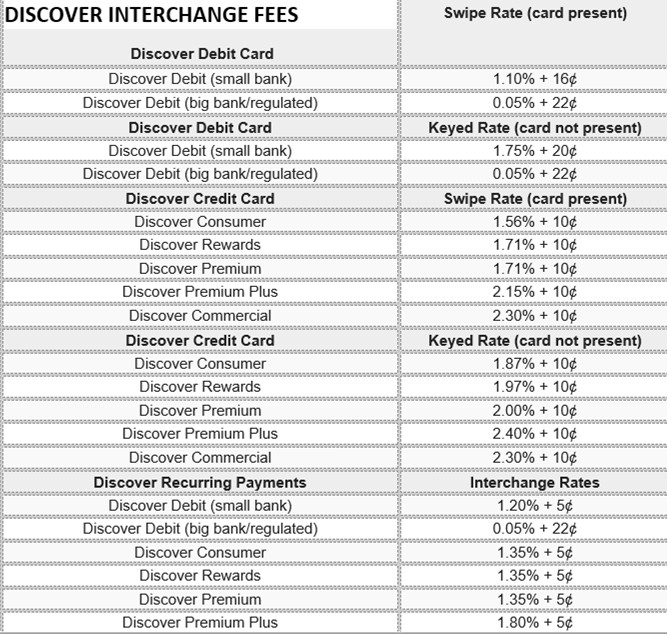

Want to save money on your merchant processing fees? Call us today!